|

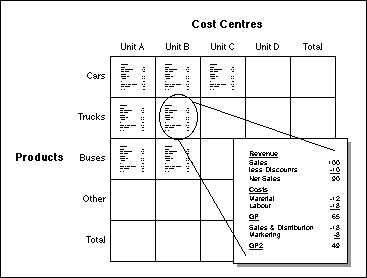

Search HansaManuals.com HansaManuals Home >> Standard ERP >> Accounting Principles >> Chart of Accounts Previous Next Entire Chapter in Printable Form Search This text refers to program version 4.0 Objects In traditional cost accounting, the classification of expenditure and the allocation of different expenses to departments, products, regions etc. is a well known problem area. In essence, there is a need to present management reports in several different views or dimensions. Normally, there are three basic dimensions used in the accounting of any business:

Conceptually, the accounting situation can be described as a three-dimensional table:

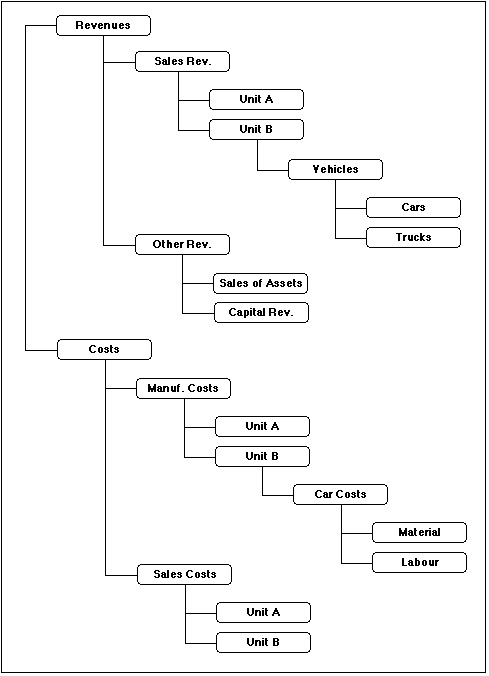

A Chart of Accounts is a list of Accounts. By definition it is one-dimensional. Through various means, the Accounts are divided into sub-classes down one or more levels, and the result is a hierarchical tree structure of classifications.

To simplify the structure many accounting systems subdivide the "account string" into different parts, each indicating cost type, department, project, product etc. This is only a half-way solution. The only logically viable solution to truly multi-dimensional accounting is to use an "Object" classification in each accounting transaction. With this method, the Chart of Accounts contains account specifications for the kind of revenue, expenditure, asset, liability or equity. Each accounting transaction consists of an Account Number, an amount, a date, and one or more Object classifications. In the example above, a wages payment for trucks in Unit C would contain the following information: Number 970001 With this classification, it will be simple to show all transactions entered for a separate product, unit and cost type, or to show a profit and loss statement for a particular section of the business. Click here for a description of how Hansa deals with this task. |