|

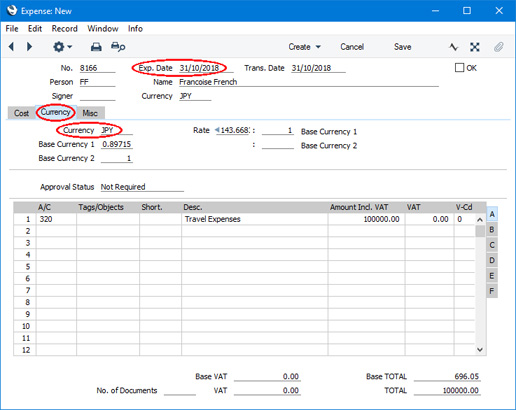

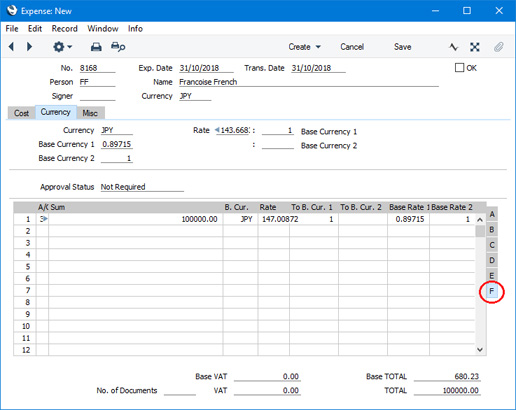

Search HansaManuals.com HansaManuals Home >> Standard ERP >> Expenses >> Expense Register Previous Next Entire Chapter in Printable Form Search This text refers to program version 8.4 Expenses in Currency When you enter an Expense record in Currency, the Currency and Exchange Rate in the header will by default be applied to every row in the Expense record. However, you can change the Exchange Rate or even the Currency in a particular row.One issue that will often arise is that the Exchange Rate on the 'Currency' card of an Expense record (i.e. the Exchange Rate applying on the Transaction Date of the Expense, which will often be the date when the expense claim was submitted) will not be the same as the Exchange Rate on the date when a transaction listed in the Expense record took place. For example, an employee submits an expense claim dated Oct 31. The claim includes a receipt for JPY 100000 (Japanese Yen) dated Oct 15, when JPY 147.00872 buys one GBP (Base Currency 1). So, the receipt was worth GBP 680.23 when it was issued. However, on Oct 31 (the date of the expense claim), one GBP buys JPY 143.66837, so JPY 100000 will then convert to GBP 696.05. Enter the Expense record as shown below. Enter the date of the expense claim (Oct 31) and the Currency (JPY) in the header:

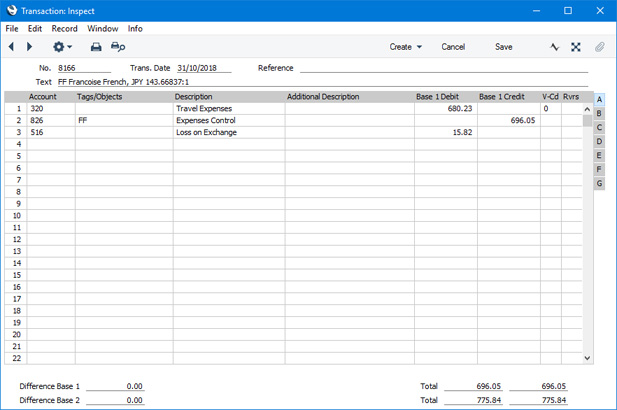

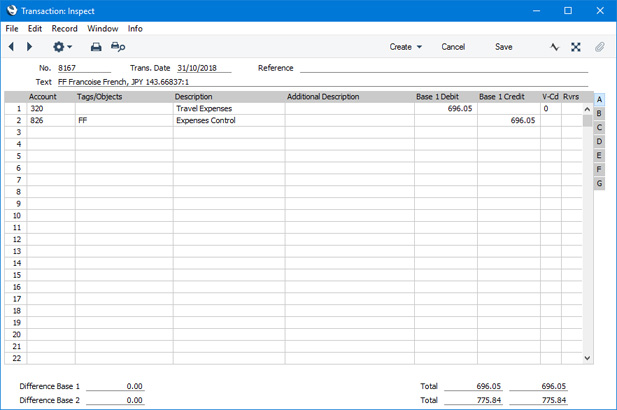

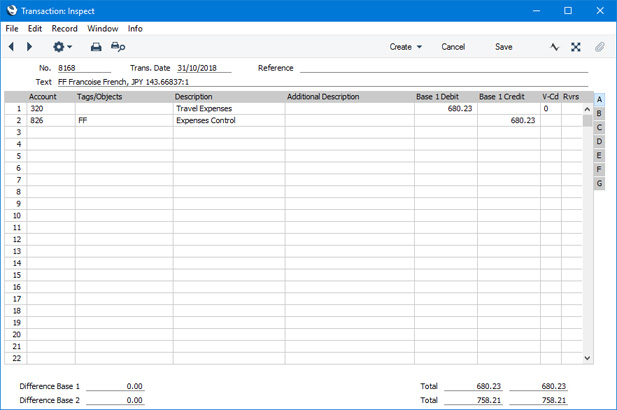

When you mark the Expense record as OK and save it, the value of the postings in the resulting Nominal Ledger Transaction will depend on the Expense Date Rate for Cost Accounting option in the Expense Settings setting. If you are using this option, the liability to the employee (Account 826 in the example) will be calculated using the Exchange Rate for the date of the expense claim (Oct 31), while the amount posted to the Cost Account (320 in the example) will be calculated using the Exchange Rate for the date of the receipt (Oct 15). The difference will be posted to the Rate Gain Account or Rate Loss Account (as appropriate) from the 'Exchange Rate' card of the Account Usage P/L setting:

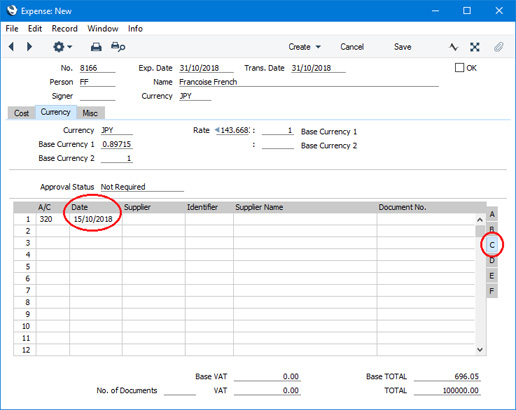

If you mix Currencies in an Expense record, you can only do so by specifying Currencies on flip F. Therefore, the Expense Date Rate for Cost Accounting option will again be bypassed. --- The Expense register in Standard ERP:

|